Admin

Admin

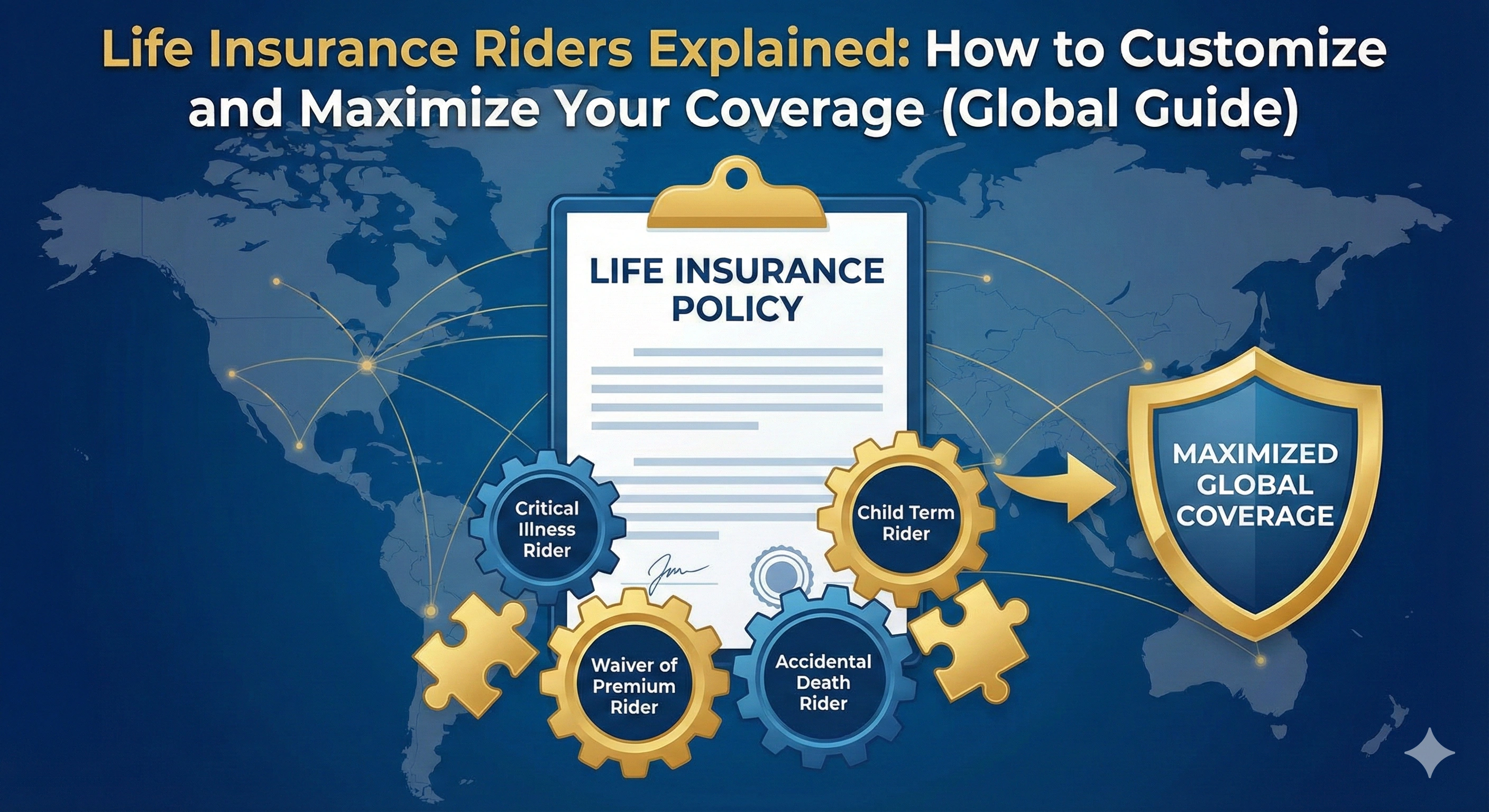

Life Insurance Riders Explained: How to Customize and Maximize Your Coverage

One of the most powerful ways to enhance a life insurance policy is by adding riders — additional benefits that provide extra protection at a relatively small cost. Riders allow you to customize your life insurance plan based on your family’s needs, lifestyle, and long-term financial goals. Whether you want coverage for critical illness, accidental death, disability, or income replacement, riders can transform a basic policy into a complete financial safety net.

This global guide breaks down the most important life insurance riders, how they work, when you should consider them, and how they help create a comprehensive protection plan.

What Are Life Insurance Riders?

A life insurance rider is an add-on feature purchased with your policy to increase coverage or provide additional financial benefits. They offer flexibility and customization, allowing policyholders to adapt coverage to specific risks.

Riders are ideal for:

- Families with dependent children

- Business owners

- High-risk professionals

- People with a history of major illnesses in the family

- Individuals seeking long-term financial security

Why Riders Are Important

Riders add tremendous value to a life insurance policy because they:

- Protect against multiple risks (illness, disability, accidents)

- Reduce the need to buy multiple separate plans

- Offer higher coverage at low incremental cost

- Provide financial support during life, not just after death

- Allow policy customization for global lifestyles

Top Life Insurance Riders (Global List)

1. Critical Illness Rider

This rider pays a lump sum if the insured is diagnosed with a major disease such as cancer, heart attack, stroke, kidney failure, or a major organ transplant. It helps cover treatment, hospitalization, and recovery expenses.

Ideal For: Families with medical history risks, working professionals, and individuals with dependents.

2. Accidental Death Benefit Rider

If death occurs due to an accident, this rider provides an additional payout to the nominee on top of the base sum assured. It is extremely valuable for people in high-travel or high-risk professions.

3. Waiver of Premium Rider

This rider protects the policy from lapsing. If the insured becomes disabled or critically ill and cannot work, all future premiums are waived, but coverage continues.

4. Income Benefit Rider

Instead of a one-time lump sum, this rider provides a monthly income to the family for a fixed duration. This helps families maintain their lifestyle after the insured's passing.

5. Terminal Illness Rider

If diagnosed with a terminal disease and life expectancy is short, the insurer pays out part of the sum assured immediately. This supports urgent medical needs and end-of-life expenses.

6. Child Education Rider

This rider guarantees that your child’s education expenses will be taken care of if the insured parent passes away or becomes permanently disabled.

7. Disability Rider

Provides financial compensation if the insured suffers partial or total disability due to an accident or illness.

8. Return of Premium Rider

If the insured outlives the term, all paid premiums are refunded. This makes term insurance feel like a savings tool.

9. Long-Term Care Rider

Helps cover long-term care costs like assisted living, at-home nursing, or chronic illness management.

10. Family Income Rider

A steady income stream is provided to the family for several years after the insured’s death.

How Much Do Riders Cost?

Riders vary in cost worldwide, but generally:

- Critical illness riders are the most expensive

- Accidental death riders are low-cost

- Waiver of premium riders are inexpensive

- Child riders cost very little

Despite the added cost, riders significantly increase the value of your policy.

Do You Need Life Insurance Riders?

You absolutely should consider riders if you belong to any of these categories:

- Parents with dependent children

- People with chronic illness risks

- Individuals with high-risk jobs or frequent travel

- Single-income families

- Business owners

- People with home loans or financial liabilities

How to Choose the Right Riders

Choosing the right set of riders involves evaluating your personal and financial risks:

1. Analyze your health and family medical history

This determines whether critical illness or disability riders are important.

2. Consider your job and lifestyle

High-risk workers benefit from accidental death and disability riders.

3. Evaluate your dependents’ needs

Families benefit from income and child education riders.

4. Compare premium impact

Add only riders that provide real value based on your situation.

5. Check global insurer rider availability

Not all insurance companies worldwide offer every rider — compare options.

Common Mistakes to Avoid

- Adding too many riders unnecessarily

- Ignoring fine print and exclusions

- Choosing a rider without evaluating long-term cost

- Assuming all riders are available globally

- Not reviewing riders annually

Conclusion

Life insurance riders are powerful tools that can customize your policy for complete financial protection. They provide additional benefits for critical illnesses, accidents, disabilities, and family income replacement—making your insurance more relevant and robust. By choosing the right combination of riders, you can build a personalized protection plan that safeguards your family today and in the future.

Take time to analyze your needs, compare global insurer offerings, and structure a policy that gives you maximum peace of mind.

Admin

Admin